Dollar Rises As Inflation Hits 3yr Highs

US CPI Jumps Again

The US Dollar continues to push higher midweek as hot US inflation and a lack of progress in US/Iran peace talks keeps USD in demand. On the inflation front, annualised headline CPI was seen rising to 3.8% from 3.3% prior, last month, above the 3.7% the market was looking for. Now back at its highest level since Q2 2023, inflation is showing no signs of shifting lower anytime soon and Fed tightening expectations were seen rising in response to the release. CME group pricing for an October hike has now risen to above 20% with pricing for a hike by year end above 35%. Given that energy prices remain near highs and are not expected to fall anytime soon, inflationary pressures could easily see CPI above 4% at the next reading. Looking ahead today, focus will be on the latest set of PPI figures which could see tightening expectations rising further if strength is seen in these readings too.

US/Iran Developments

Alongside hotter-than-forecast inflation data, USD is also staying bid through stronger safe-haven demand as traders nervously monitor US/Iran peace talks. Hopes for a deal ahead of Trump’s meeting with Xi this week have been dashed and with rhetoric from both sides turning more hostile again, uncertainty is rising. For now, USD looks likely to drift higher with any hawkish Fed commentary this week seen further supporting demand.

Technical Views

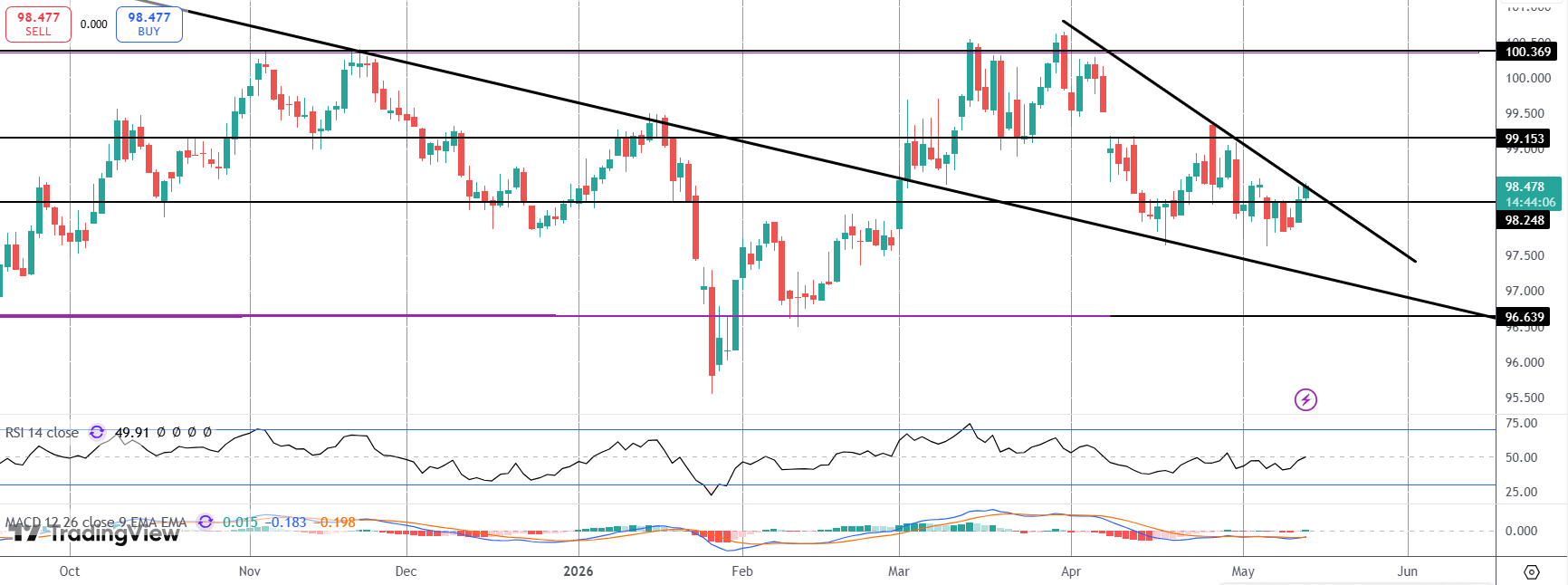

DXY

The Dollar is now testing the falling edge top, probing above 98.24 also. If we break higher here, focus will turn to 99.15 as the next resistance to note ahead of the bigger 100 level above. If we break back below 98.24 near-term, 96.63 is the deeper support level to note.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

With 10 years of experience as a private trader and professional market analyst under his belt, James has carved out an impressive industry reputation. Able to both dissect and explain the key fundamental developments in the market, he communicates their importance and relevance in a succinct and straight forward manner.